To learn more about BlueVine and decide if it’s right for your needs, please continue reading:

Few online business lenders are as highly regarded as Bluevine. If you were to research their products, you’d quickly be greeted by many glowing reviews, and for a good reason. For starters, Bluevine offers virtually all the advantages you’d expect from a reputable online business lender. Their products are easily accessible for younger, smaller businesses, especially those with subpar personal credit. Even Bluevine’s fee policies are considered optimal compared to the rest of the industry.

However, certain cash flow situations call for different products, and some businesses might not meet Bluevine’s requirements or fulfill their repayment structures. This guide will discuss what separates Bluevine from other popular online lending options.

Specifically, we’ll answer these questions and more:

Bluevine is a financial technology company specializing in small business financing. The company’s ownership started Bluevine in 2013. Bluevine offers business checking accounts and business credit cards. Bluevine delivered more than $13 billion in financing to more than 425,000 business customers.

The online-only lender has lightning-fast funding times, making it an attractive option for small business owners needing urgent working capital. Bluevine’s rates are consistent with similar lenders.

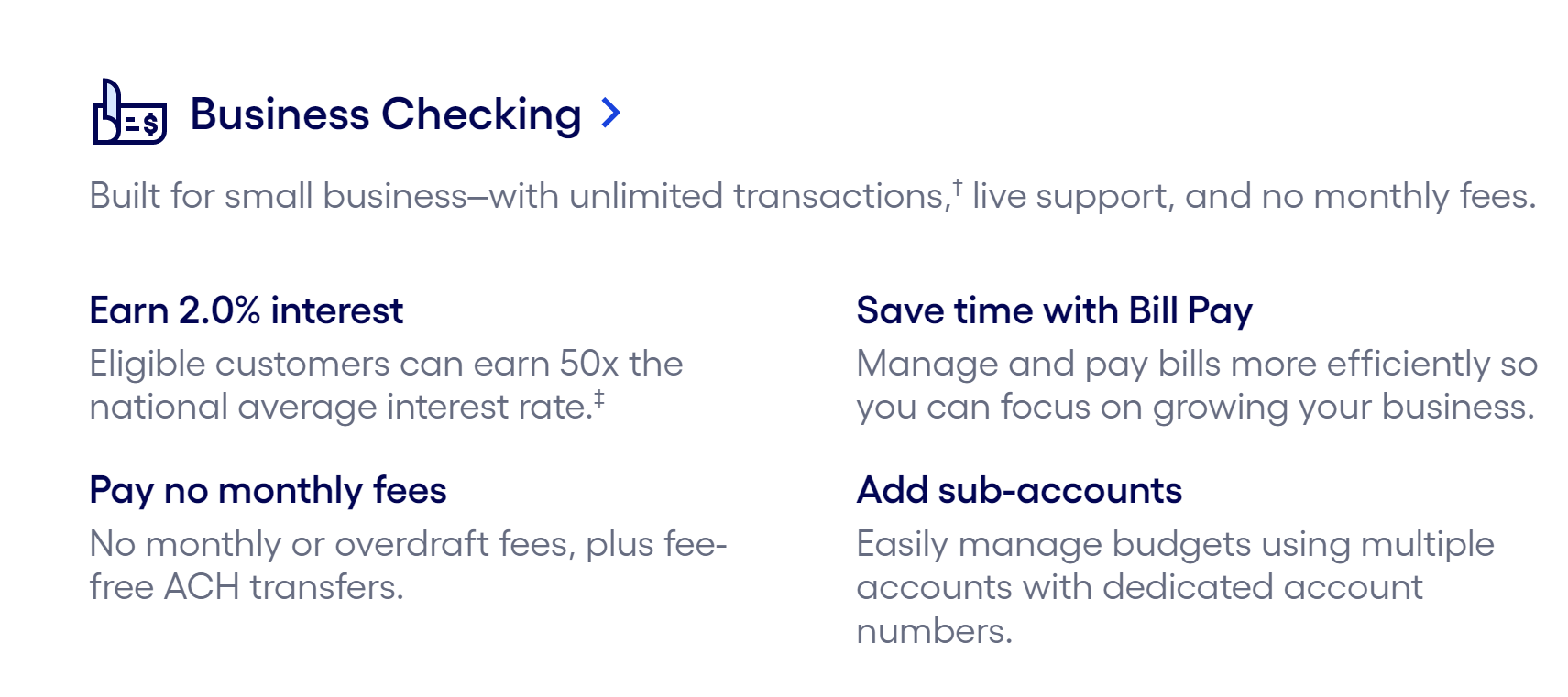

In addition to short-term financing options, Bluevine also offers a business banking platform tailored for small businesses. This platform emphasizes personalized customer service and expert guidance, ensuring small business owners receive the support they need. Their business checking account product comes with several advantages for small business owners.

Bluevine is renowned for its outstanding customer service and support. The company’s representatives are readily available to address any questions or concerns, and many customers have praised their responsiveness and knowledge.

Bluevine also provides various resources and tools designed to help credit customers manage their accounts effectively. Whether you need assistance with account setup, have inquiries about fees and charges, or require help with a specific transaction, Bluevine’s customer service team is dedicated to ensuring a smooth and satisfactory banking experience.

As a financial technology company, Bluevine prioritizes transparency and fairness in its fee structure. The company offers a range of business checking accounts with no monthly fees, making it an attractive option for small businesses. Many of Bluevine’s services are either free or come at a low cost, ensuring that small business owners can manage their finances without worrying about hidden charges.

Additionally, Bluevine’s line of credit features competitive interest rates and no hidden fees, providing a clear and straightforward borrowing experience. All fees and charges are clearly outlined on Bluevine’s website, allowing customers to make informed decisions about their banking needs.

Bluevine stands out from traditional banks by offering a range of innovative banking services tailored specifically for small businesses. As a financial technology company, Bluevine is not bound by the same regulations as traditional banks, allowing it to provide more flexible and competitive products. For instance, Bluevine’s business checking accounts offer higher interest rates and lower fees compared to many traditional banks.

The user-friendly banking platform is designed to be accessible, enabling small business owners to manage their finances efficiently, even on the go. Overall, Bluevine’s unique approach to banking provides small businesses with the tools and flexibility they need to thrive in today’s fast-paced market.

Bluevine started as an invoice factoring company but pivoted into other small business loans. However, they discontinued their term loan product and now use another financial institution for invoice factoring.

Bluevine started as an invoice factoring company but pivoted into other small business loans. However, they discontinued their term loan product and now use another financial institution for invoice factoring.

Bluevine’s business credit card allows users to earn unlimited 1.5% cash back on purchases. Bluevine accounts are FDIC-insured through Coastal Community Bank. Bluevine allows for account management from a single platform for checking accounts and associated features.

Bluevine’s main product is now their business line of credit, which goes up to $250,000. The terms for the line of credit are either 6 or 12 months. The company is not a bank and partners with Celtic Bank, member FDIC, to provide its line of credit.

Bluevine no longer provides invoice factoring. The company sold its invoice factoring division to FundThrough. Current Bluevine customers with invoice factoring had their accounts switched over the FundThrough. New applicants apply directly to FundThrough.

While it’s not a financing product, Bluevine does offer a convenient, FDIC-insured online business checking account as part of its business banking platform tailored for small businesses. The platform emphasizes personalized customer service and expert guidance, ensuring that businesses benefit from dedicated support and effective features. Bluevine offers high interest rates on checking accounts and no monthly fees.

To qualify for a business line of credit through the Bluevine platform, you’ll need the following:

To be eligible for a Bluevine business line of credit, applicants must show a minimum annual revenue of $100,000. Bluevine’s line of credit can carry terms of six or twelve months. For the latter option, you’ll need a credit score of at least 620, at least two years in business, and at least $450,000 in annual revenue. The minimum personal credit score required for a Bluevine business loan is 625.

Bluevine does not work with businesses located in North Dakota, South Dakota, or Vermont. Businesses with tax liens can be approved if the company is currently on a repayment plan. However, tax liens may prevent applicants from accessing more significant borrowing amounts. If you have previously declared personal bankruptcy, you can be approved if the bankruptcy was discharged at least one year ago.

Applicants for lower borrowing amounts may have to sign a personal guarantee. If you default, Bluevine can seize your personal assets to compensate for the loss.

Bluevine’s interest rates can vary tremendously, depending on factors like credit score and overall financial health. Business lines of credit interest rates range from 4.8% to 51%. Bluevine’s business loans are available to businesses across the country.

The minimum borrowing amount for the business line of credit is $5,000. Borrowers can repay credit lines weekly or monthly, depending on the terms.

Payments for all Bluevine products are reported to Experian. Thus, making timely payments will improve your business credit score. There are no annual fees, monthly fees, or origination fees for all three products.

To apply online for a Bluevine line of credit, you will need the following:

Like many online business lenders, applying for a Bluevine credit line involves a short application that can be completed in just a few minutes. Here’s how to get started:

You can apply for Bluevine products through United Capital Source. The UCS online application requires basic information about you and your business. After entering this information, Bluevine will perform a soft pull on your personal credit score. According to Experian, soft inquiries do not impact your credit scores.

After submitting your application, Bluevine will get back to us with an offer anywhere from five minutes to 24 hours (one business day). UCS will help negotiate rates and terms to ensure you receive the most beneficial arrangement for your business.

If you choose to accept the offer, Bluevine will perform a hard credit pull. You can then sign your loan documents and decide how to receive the funds. If you pay $15 for a wire transfer, Bluevine will deposit the funds in your bank account in just a few hours. If you choose not to pay, it could take up to three business days to get funded.

Bluevine will charge you a 1.6% to 2.5% draw fee for a business line of credit every time you draw funds. Bluevine will also review your business’s debt before allowing you to use your line of credit. For this reason, Bluevine may deny your request to draw funds if you’ve accrued too much new debt.

Repayment terms are either 6 or 12 months. If you have a six-month term, Bluevine will automatically deduct 26 weekly payments from your bank account. You will make twelve automatic monthly payments if you have a twelve-month term.

Since this is a revolving line of credit, the funds you repay become available to you again. For example, let’s say your weekly payment is $200, and your fee is $10. In this case, paying back that $200 will increase your credit line by $190.

Once you accept an offer, Bluevine will file a blanket UCC lien on your business. Bluevine may also be able to refinance up to 100% of your existing debt.

Bluevine easily fulfills some of the main advantages businesses look for in online business lenders. It’s not uncommon for borrowers to receive funds in a matter of hours. Other business lenders might take closer to a few days to distribute funding. Their application process is also speedy and requires minimal paperwork. This makes Bluevine very attractive for businesses that need money now, not next week.

BlueVine’s business banking platform is tailored for small businesses, offering personalized customer service and expert guidance to meet their unique needs.

Another significant advantage is Bluevine’s low minimum credit score. While other business lenders have minimums closer to 650, Bluevine approves lines of credit for credit scores as low as 600.

As a provider of short-term financing, it’s no surprise that Bluevine prioritizes accessibility and convenience.

Bluevine’s most significant disadvantage is its prices. All their products are costly compared to the business financing industry. It’s risky to lend to younger businesses with poor credit. Hence, Bluevine attaches high interest rates to offset the heightened risk. But high interest rates should be expected with any business lender with such loose requirements.

However, while many online business lenders charge higher rates, very few require weekly payments. This payment frequency might not work for businesses that don’t maintain considerable bank balances throughout the month.

Between the size of your payments, the payment frequency, and the draw fee for a line of credit, Bluevine’s repayment structure could put pressure on your cash flow.

Pros:

Cons:

Bluevine’s high rates might give the impression that they do not have their client’s best interests at heart. However, high rates generally come standard with short-term financing. And since Bluevine works with clients with bad credit and little time in business, high rates ensure they can continue supporting themselves should their clients run into financial trouble. These rates are also a logical drawback to applying for and accessing funds within 24 hours.

Any suspicions about Bluevine’s legitimacy can be quelled by its A-plus rating from the Better Business Bureau (BBB) and its myriad positive reviews. Bluevine has received multiple industry awards and recognition for its technology and partnerships with small businesses.

You should never pursue an online business funding product that you aren’t sure you can afford. But if you’re worried that Bluevine’s rates and weekly payments could impact your cash flow, your instinct may be correct. For this reason, you might want to contact Bluevine and explain your financial circumstances to ensure this is the right product for you.

Bluevine is rated “Great” with 4.2 / 5 on Trustpilot. Users report that Bluevine’s dashboard is clean and simple to use.

Many Bluevine clients praise the simplicity of the application process. Bluevine reviews also tend to revolve around their quality customer service. Since Bluevine is an online business lender, new clients might be caught off guard by how easy it is to speak to a human representative. Additionally, many customers have had positive experiences with BlueVine’s business banking platform, highlighting the personalized customer service and expert guidance they received.

Customers report receiving in-depth assistance from Bluevine representatives during onboarding and account management. Bluevine representatives are responsive to customer needs and provide timely follow-ups during account management. Many users mentioned their Bluevine rep by name. Here are a few highlights:

“Branden provides excellent customer service by explaining all of the benefits of accounts and making sure clients understand how to use them.”

“Colby Gluck is professional, knowledgeable, and dedicated to answering all customer questions during the service process.”

“Janice is exceptional at understanding her product and is very patient during the setup process for new customers.”

Some reviews came from new clients who were unaware that Bluevine examines your business’s debt every time you try to draw funds from your line of credit. Unfortunately, business lenders might not disclose policies of this nature unless you ask. That’s why you should always ask about potential restrictions on your drawing ability before accepting a new line of credit. There are reports of slow responses from Bluevine’s customer service in certain situations, leading to frustration from customers.

Bluevine is one of the few online business lenders that reports your payments to a major credit bureau, regardless of which product you choose. Hence, using Bluevine products successfully will raise your business credit score—specifically, Bluevine reports to Experian.

Bluevine might decline your application after determining that your cash flow cannot handle your desired product’s cost or repayment structure. The six-month line of credit requires weekly payments. To satisfy this repayment structure, your cash flow must be very consistent. Occasional dips in revenue or cash flow shortages could make it difficult to pay the same amount every week.

Sometimes, they might decline an application if the small business owner has poor credit. In that case, they’d have to look for bad credit business loans from other providers.

Thankfully, plenty of other online business lenders offer more flexibility with their repayment structures. The application process is just as quick as Bluevine’s, and their requirements are comparably loose. Even younger businesses with poor credit can choose between daily, weekly, bi-weekly, or monthly payments. You may also be able to access longer terms instead of Bluevine’s 12-month limit.

If you’re interested in accounts receivable factoring or a business line of credit, you shouldn’t have trouble finding another business lender that gives your customers more than two weeks to pay.

Online business lenders tend to get lumped together. At first, it seems like they all offer the same products for the same types of businesses. But as you can see, companies like Bluevine have unique requirements, borrowing limits, terms, and repayment of the right product for your business.

Here at UCS, we know that many of our clients utilize Bluevine’s services and are satisfied with the financing structure. These are the kinds of details potential clients must keep in mind when examining their options.

Different online lenders and business financing products suit different types of cash flow. The more you know about your individual goals and challenges, the easier it will be to find the lender for your needs.

We know that Bluevine customers continue to work with them for multiple rounds of financing. For this reason, we give them a 4.8 out of 5 rating, one of our highest ratings for lenders we work with.

Disclaimer: The Bluevine trademark is owned by Bluevine Inc. and its use herein is for reference purposes only and it does not indicate sponsorship or endorsement from Bluevine Inc.