| THE COMPETITION | ||

|---|---|---|

| Point Of Sale Operating Costs | As low as $89/monthly | $5,000 – $7,000 per system |

| System Access | Free back office solution. Allows access from any computer with an internet connection. | POS access limited to dedicated back-office PC, which adds additional cost |

| Installation Cost | Onsite installation and advanced remote training included. | Typically offered at additional cost |

| Point Of Sale Operating Costs | Next day funding available on credit/debit purchases* | 2 to 5 business days for funding is the industry standard |

| Warranty | 3 year warranty on all hardware | Merchant is responsible for any replacement costs |

| Programming | Menu/Inventory programming | Typically offered at additional cost |

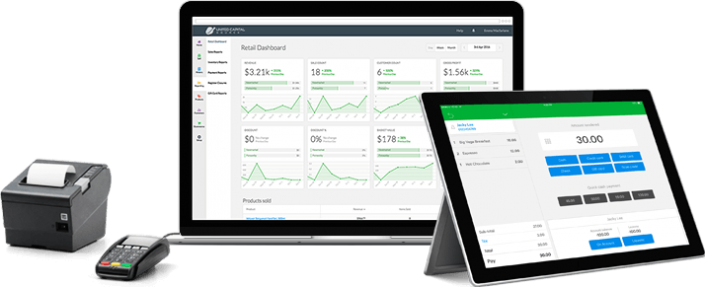

| Point Of Sale Hardware Included | Two hardware options including our new all-in-one terminals and proven, industry specific software | Hardware and software vary by company |

| Additional Benefits | Internal NO FEE gift and loyalty program | Gift cards may be available at an additional cost |

| Dedicated Support | 24/7/365 in-house customer support | May or may not be available. 24-hour support generally requires an extra cost |