These are the best bad credit business loans available:

As you can see, the only small business loans offered by UCS missing from this list are Business Term Loans and Small Business Administration (SBA) Loans. This is because once business term loans or SBA loans lose their traditionally high borrowing amount, low interest rate, and long term, it essentially becomes a short-term small business loan or a product similar to invoice financing (get paid upfront on unpaid invoices) and merchant cash advances. SBA and term loans are considered the best small business loans, carry the lowest interest rates on the market, and are only available to small business owners with high personal credit scores.

Unlike an SBA or term loan, every one of the small business loan options on this poor credit list can be repaid quickly and provide a modest amount of funding at best. In addition, small business owners can choose from various alternative lenders and financing options rather than being forced into fixed monthly payments. Even short-term business loans can be repaid weekly, bi-weekly, or monthly.

Some bad credit small business loans emphasize cash flow and sales volume rather than low credit scores. For example, your borrowing amount for a merchant cash advance is based entirely on monthly debit and credit card sales. With accounts receivable factoring and invoice financing, your personal credit score is largely irrelevant. Invoice factoring can help businesses access cash quickly by selling unpaid invoices to a factoring company.

Revenue-based business loans have similar personal credit score requirements as a merchant cash advance, except the loan amount is based on your total monthly sales, not just credit cards and debit transactions.

Business lines of credit are also available with poor credit scores. However, the terms won’t be as favorable as a small business line of credit from your local bank. Small business owners with poor credit or limited business credit scores can still have access to revolving lines of credit if that’s the best bad credit product that suits their business needs.

And though business equipment financing carries the same repayment structure as a term loan, the desired equipment is used as collateral. This decreases the heightened risk associated with a poor credit history and personal credit score.

When it comes to business loans, a personal credit score can have a significant impact on the approval process. Lenders often use personal credit scores to evaluate the creditworthiness of a business owner, especially if the business is relatively new or has a limited credit history. A good personal credit score can increase the chances of getting approved for a business loan, while a bad credit score can make it more challenging.

Here are some ways a personal credit score can impact business loans:

Overall, a good personal credit score is essential for business owners who want to increase their chances of getting approved for a business loan. By maintaining a good credit score, business owners can access better loan terms, lower interest rates, and more favorable repayment periods.

Nearly 65% of medium and high-risk credit applicants received at least partial approval when applying to an online lender. Source: 2023 Small Business Credit Survey

55% of business loan applicants at online lenders stated that speed or credit decisions were the primary motivating factor. Source: 2023 Small Business Credit Survey

Generally, most traditional lenders require a minimum personal credit score of 650 for approval. And most lenders of traditional business credit loans and lines of credit prefer a minimum personal credit score of 680. Source: Experian

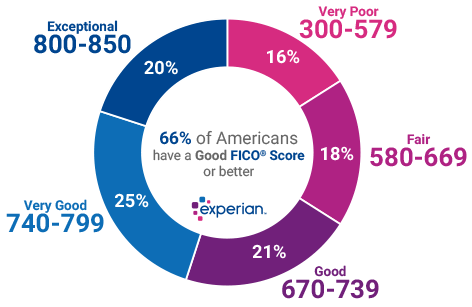

Bad credit is generally defined as a FICO score between 300 and 629. Credit reporting agencies break it down like this:

Several criteria come into play when traditional lenders review small business loan applications. However, they do pay special attention to credit scores. (Note: there are different types of credit scores. Many traditional lenders use FICO scores, developed by The Fair Isaac Corporation, to assess personal and business borrowers’ creditworthiness.)

Your credit score is a number that represents how likely you are to pay back your small business loans. It’s based on your previous credit history. Lenders look at business owners’ personal credit scores before offering credit to new small businesses or if a personal loan guarantee is required.

Credit reporting agencies calculate credit scores based on what’s known as “The 5 C’s of Credit.” They include

Offer Collateral – To boost the likelihood of getting a “yes” to a small business loan with a bad credit score, offer collateral as security. This could be equipment or your accounts receivable to a factor, customer invoices for invoice financing, or future credit card sales.

When underwriters assess business owners with bad credit history, they look at other factors, in addition to the minimum credit score, to determine their ability to repay. These other factors include:

The last item on this list stems from the fact that bad credit may be more common in small businesses in specific industries. Your industry also gives us an idea of which repayment structure works best for your cash flow.

Time in business is at the top of the list because it shows that you’ve managed to get your business out of financial dilemmas before. In other words, you’re more likely to repay a loan when you have more experience keeping your business alive during desperate times. Many companies make money, but only some stay in business for years.

As for collateral, it’s important to remember that business lenders usually do not accept your assets’ full monetary value as security. For example, let’s say your collateral is worth $10,000. That might be enough to secure a $6,000 business loan or line of credit.

Generally, our network of alternative lenders doesn’t need collateral for most programs. Instead, business loan terms are structured differently for those small businesses that have owners with a poor credit history. A business credit card also requires no collateral in most cases.

There are many benefits to getting a business loan when you have bad credit. If you choose a short-term small business loan, just a few months’ worth of payments can dramatically raise your business credit score. This is a much more effective and efficient way to offset previous credit issues than getting something removed from your credit profile. Business lenders and potential business partners would rather see a previous credit issue followed by a paid-off loan than nothing at all.

When you get a business loan, you can create a new payment history. This record of timely payments shows that you’re no longer the kind of person who misses payments or defaults on loans.

A business loan also gives you another funding source, so you don’t have to continue using other sources, like your credit card. One key factor for determining your credit score is your credit utilization rate. This reflects how much of your available credit you use. If you use your credit cards too much (or nearly max them out), your utilization rate gets too high and keeps your credit score down. Thanks to a business loan (and alternative lenders), you can only finance certain expenses with the credit limit on your business credit card and keep your utilization rate low.

Online business lenders can offer funding options with less stringent requirements compared to traditional banks. Traditional lenders often want businesses in operation for at least two years and prefer good credit applicants. Alternative lenders have become more popular due to their flexible credit requirements for business loans.

Payments for most working capital loans, equipment financing, and a business line of credit usually get reported to business credit bureaus. The other types of business loans for bad credit are much easier to repay because payments are deducted automatically. Most often, your payment history for these loans will not impact your business credit score.

If raising your score is a top priority, check how often payments are reported. It can take 30 to 90 days for the information reported to a business credit agency to appear on your report. The sooner your reported payments appear on your report, the quicker you raise your credit score.

Using inventory as collateral can help you get a small business loan with bad credit. However, this strategy only works under certain conditions:

The type of inventory matters, as well. Different types of inventory are easier or harder to sell in the event of default. This is reflected in the inventory’s liquidity. The easier it is to sell, the more of its value you can borrow.

Small businesses borrow money for a wide variety of reasons, including

While bad credit business loans can provide necessary funding for businesses with poor credit, there are alternative options available. These alternatives can offer more favorable terms, lower interest rates, and fewer fees. Here are some alternatives to bad credit business loans:

These alternatives can provide businesses with poor credit with more favorable funding options. However, they may have their own set of requirements and limitations. It’s essential to research and compare these alternatives to find the best option for your business needs.