A fast-funding small business loan is financing that can be approved and deposited in 1 to 3 business days, usually through an online lender or an alternative financing provider. Speed depends on how quickly your bank statements are verified and how clean your documentation looks. Most delays come from missing paperwork or identity mismatches, not from lenders moving slowly.

A working capital loan is business financing used to cover day-to-day operating expenses—such as payroll, rent, inventory, and vendor bills—rather than long-term assets like real estate. You receive a lump sum and repay it over a fixed term, usually with daily, weekly, or monthly payments. This is different from a business line of credit, which provides a revolving spending limit

Quick MCA Requirements for 600 Credit Score (One-Screen Summary) Bank denial is common. Banks underwrite based on fixed-payment affordability and often require higher credit scores, collateral, and tax returns. MCAs are primarily revenue-based. If your credit score is around 600 and your deposits are steady, your bank statements—not your FICO—usually determine whether you’re approved for an MCA and what it

Same-week MCA funding is usually a documentation and verification issue, not a credit-score issue. Your deposits and trends matter more than your FICO. Understanding the difference between approval, contract signing, and funding disbursement is critical.

Approval means an underwriter reviewed your statements and offered terms. Contract signing means you agreed to the factor rate, holdback, and total payback. Funding

If you need financing for your business in 2026, understanding current SBA loan interest rates can save you thousands of dollars. In 2026, SBA 7(a) interest rates are generally priced as a base rate (usually Prime) plus a lender spread, with SBA-set maximum caps that depend on loan size and whether the rate is fixed or variable. This guide provides

Financing a mobile or manufactured home community involves obtaining loans to purchase or improve the property. Lenders consider factors such as the park’s location, condition, and revenue potential. Government agencies may also provide assistance or financing options for these communities.

Lenders may offer various financing options, including traditional real estate loans, government-backed loans, or specialized mobile home park loans. The

Alternative business financing refers to funding options for businesses outside traditional bank loans. Non-bank lenders, such as online lenders, peer-to-peer lending platforms, and crowdfunding websites, typically offer these alternative financing options. These lenders provide access to capital for businesses that may not qualify for a bank loan due to factors like limited credit history, short time in business, or unconventional

In most cases, a business line of credit won’t directly impact your personal credit score. Most commercial lenders only report the business credit bureaus, such as Dun & Bradstreet or Experian Business.

That means business line of credit activity won’t appear on your consumer credit reports from the three major consumer credit bureaus: Experian, Equifax, and TransUnion. This is

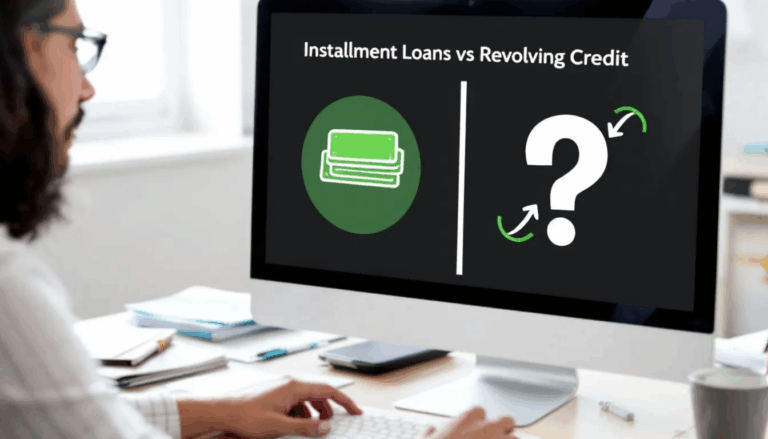

When deciding between a revolving credit line and an installment loan, businesses must carefully consider their specific needs and financial situation to determine the right choice. Here are some factors to consider.

Using business credit to purchase real estate offers several advantages. Firstly, it allows businesses to separate personal and business finances, enhancing financial organization. This separation is crucial for maintaining clear records and simplifying tax filings.

Moreover, leveraging business credit for real estate acquisitions can significantly boost a company’s purchasing power. By accessing additional funds through credit lines or loans, businesses